Kindness, hope, sun and horizon are the names of some of the banks’ facilitation plans whose billboards have been hanging on the city walls for some time. Plans that were supposed to provide micro-facilities to ordinary users. But in fact, there is no news of a new validation model in any of these plans, and still no loan guarantor.

Please bring a guarantor

Although the activists of the central bank never provided a precise definition of the new validation model, but if we consider the definition of Abuzar Soroush, the deputy supervisor of the central bank, that the scope of the new validation system is not limited to the banking network, or the statement of the Minister of Economy, Ehsan Khandouzi, about abandoning the model Use the ineffectiveness of past validation as a criterion. It seems that there was no change in this pattern in 1402, and most people and companies still do not have the possibility to receive facilities.

For example, in the Mehrabani loan plan of the Melli Bank, the applicant needs a valid guarantor and a valid pay slip to receive the loan, and the banks’ definition of credit is still government officials. In the next condition of receiving a loan in this facility, it is stated that the applicant must have an account in the Melli Bank and place his deposit in the Melli Bank for 1 to 12 months. The longer the deposit period, the higher the loan amount. The ceiling of the loan amount is 300 million Tomans.

Melli Bank has not been very kind!

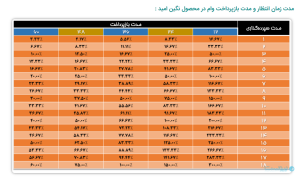

According to the loan calculation table that Melli Bank has placed in the Baam application, users can enter the required amount of their loan in the table and know the amount of their loan by setting the repayment time and deposit time. For example, if a user is applying for a loan of one hundred million tomans, he must save 128 million tomans in his loan account for 6 months and return it to the bank after two years.

A possibility that is not available for many users and has brought many users protest on social networks. One of these tweets said: “For a 300 million loan, you must have 600 million tomans, and of course, you do not need the interest and principal of your money for 6 months. Don’t forget the guarantor. “It seems that the Melli Bank is not very kind.”

In the Aftab Bank Sina plan, just like in the Mehrabani plan of Melli Bank, there is no kindness, light and warmth. If a customer needs a loan of 300 million tomans, he must deposit a larger amount than the loan principal for at least one month to one year, and the Omid plan Sepe Bank has acted more disappointingly than these two plans. Sepah Bank’s Negin Omid plan is in such a way that the period and the average deposit amount are the criteria for the loan amount that users can use in the future, and the common feature of all these loans is the duration of the deposit and having a government guarantor.

What is the new validation model?

But the thing that has not been given a precise answer in the meantime is that what is the exact definition of the central bank activists of the new validation model? Mehran Moharamian introduced the new validation at the Seed of Hope meeting last year, a combination of the current method and new methods and said: With the data given to the Iranian Validation Company, we will witness a new form of validation. In this form, in addition to ranking, reporting is also on the agenda. In other words, the new form of validation is a combination of current methods and new methods. In the most optimistic situation, between 30 and 40% of people have validation points and over 70% of people do not have validation information at all, it seems that there is a long way to implement new validation methods.

Finally, it seems that currently only Bluebank Saman and wepod Bank of Pasargad have provided facilities to their customers by relying only on validation and without guarantor, check or promissory note, and now that the central bank has restricted Landtechs has given up. We have to wait and see if the players in this field can continue on their way?

No Comment! Be the first one.